U.S. oilfield services company Weatherford International Plc on Dec. 29 sold a U.S. oil-well business to rival Schlumberger NV for $430 million, abandoning a planned joint venture.

Source: Daily Dose of ShaleDirectories.com News

Saturday, December 30, 2017

Friday, December 29, 2017

Looking Back at the 10 Biggest Shale-Related Storylines of 2017

What a difference a year can make.

Although that saying is about as cliché as it gets, it perfectly sums up a strong 2017 for the U.S. oil and natural gas industry on numerous fronts. Following some rough sledding from late 2014 through 2016, the shale industry not only enjoyed a resurgence this past year — it is clearly in the early stages of a new revolution that has been described as Shale 2.0. Here’s a look back at the top-10 shale-related storylines of 2017.

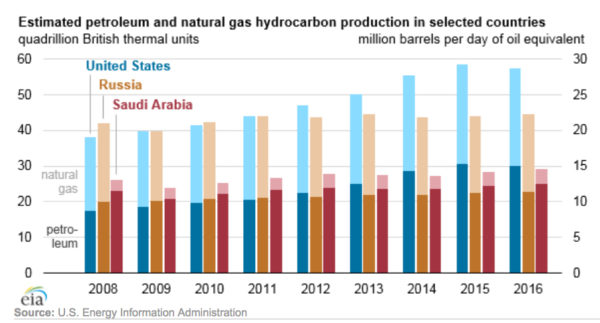

1. U.S. Cements Status as World’s Top Oil & Gas Producer, Poised for Record Production

Not only did the U.S. retain its status as the world’s largest oil and natural gas producer for the fifth straight year this past year (see chart below), it became clear in 2017 that this is a title we won’t soon relinquish.

Emboldened by OPEC’s unconditional surrender following its failed failed price war — and bolstered by the improved technology and efficiency that war necessitated — U.S. shale producers pushed domestic oil production up by more than 650,000 barrels per day (b/d) between January and September of this year.

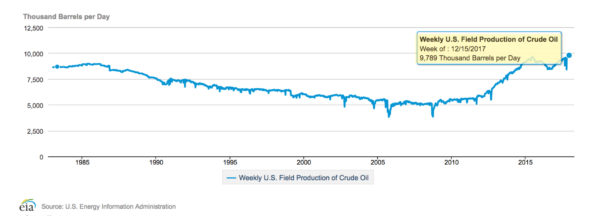

Weekly production actually reached record levels seven weeks in a row in the final two months of the year, as the following Energy Information Administration (EIA) chart illustrates.

The EIA now forecasts U.S. oil output will surpass 10 million b/d in 2018, shattering the all-time record set in the early 1970s, thanks to a nearly 1.2 million b/d increase in oil production from shale development alone in 2017.

This incredible production growth can be traced to higher (and more stable) commodity prices in the wake of OPEC’s surrender, and the fact that the average shale oil breakeven price has dropped an incredible 42 percent since 2013, according to a recent World Bank report.

A similar success story has developed on the shale gas front. Between January and December of this year, U.S. shale gas output grew from about 47.6 billion cubic feet per day (Bcf/d) to more than 62.2 Bcf/d — a near 31 percent increase. Natural gas output from shale is projected to grow even further in 2018, with the EIA estimating an increase of 764 million cubic feet per day (MMcf/d) from December 2017 to January 2018, as production gains continue to be driven by the surging Appalachian Basin.

Energy expert Dr. Agnia Grigas might have summed it up best earlier this year when she said that we are in the midst of the “golden age” of American natural gas.

And incredibly, the International Energy Agency (IEA) recently released a report that forecasts U.S. oil and natural gas production increasing 50 percent higher than any country has ever achieved over the next decade, cementing America’s status as the “undisputed leader” in global oil and natural gas production.

2. Record Oil and LNG Exports

Even more stunning than the U.S.’s march toward shattering all-time record for oil and natural gas production was the fact that we achieved record oil and natural gas exports in 2017.

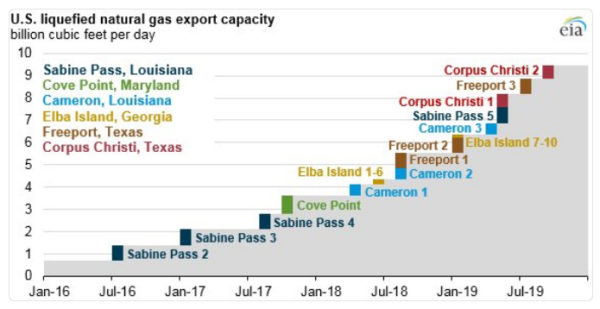

According to the EIA, U.S. liquefied natural gas (LNG) exports averaged 1.9 Bcf/d through November of this year, something almost unthinkable a decade ago when the U.S. was importing more than 3 Bcf of LNG per day. Moreover, U.S. LNG export capacity increased from about 1.5 Bcf/d in January to roughly 2.8 Bcf/d by the end of the year. U.S. LNG export capacity expected to nearly quadruple by 2019 as additional terminals come on line, as the following EIA graphic illustrates.

Spurred by this LNG export growth, the U.S. not only became a net exporter of natural gas for the first time in nearly 60 years in 2017, it is on a clear path to becoming the world’s leading LNG exporter in the not-so-distant future.

Spurred by this LNG export growth, the U.S. not only became a net exporter of natural gas for the first time in nearly 60 years in 2017, it is on a clear path to becoming the world’s leading LNG exporter in the not-so-distant future.

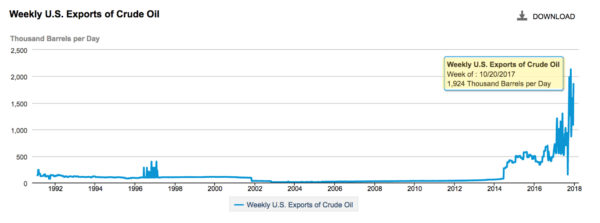

Similar to LNG exports, U.S. crude exports have gone from essentially being non-existent to approaching a record 2 million barrels per day (mbpd) in 2017.

As impressive as these figures are, an even more important storyline is the fact that booming U.S. oil and natural gas exports have not have not caused domestic energy prices to spike, as many naysayers claimed would happen.

As impressive as these figures are, an even more important storyline is the fact that booming U.S. oil and natural gas exports have not have not caused domestic energy prices to spike, as many naysayers claimed would happen.

Americans are actually enjoying record low energy prices, as residential, industrial and commercial natural gas costs have fallen since 2010. Residential natural gas prices have dropped dramatically in places like Pennsylvania (40 percent decline) and West Virginia ($4.3 billion decline) since shale development began.

3. U.S. Emissions Continue to Decline Even as Production Skyrockets

Data released in 2017 confirm beyond a shadow of a doubt that the U.S. is not only the world’s top oil and gas producer, we are also leading the world in greenhouse gas reductions.

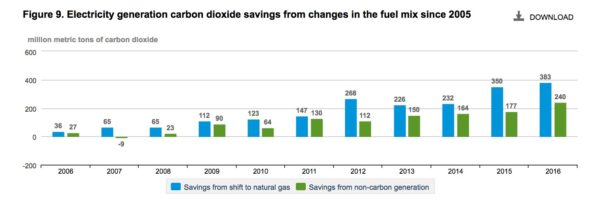

The latest EIA data show that energy-related CO2 emissions fell 1.7 percent in 2017 and are at their lowest levels in a quarter of a century. The U.S. has reduced energy-related carbon emissions 14 percent since 2005 — a trend that can be largely credited to increased natural gas use for electricity generation, and you don’t have to take our word for it.

EIA published data this year showing that 63 percent of the 3,176 million metric ton (MMT) drop in CO2 emissions from 2005 to 2016 can be directly attributed to switching to natural gas for electricity generation. Overall, shifting to natural gas for power production has resulted in a 2,007 MMT reduction in CO2 emissions since 2005, almost twice the amount that can be attributed to renewable energy sources.

It is with these facts in mind that United Nations Energy Programme chief Erik Solheim recently said, “In all likelihood, the United States of America will live up to its Paris commitment, not because of the White House, but because of the private sector.”

But what about the methane leaks that anti-fracking activists claim wipe out natural gas’ climate benefits? The latest U.S. Environmental Protection Agency (EPA) data also refutes the “Keep It In the Ground” movement’s favorite go-to claim that oil and gas production are driving up methane emissions and exacerbating climate change.

A recent EID report based on EPA Greenhouse Gas Reporting Program (GHGRP) data finds that methane emissions from major onshore oil and natural gas production facilities declined by nearly 14 million metric tons between 2011 and 2016, and have declined in virtually every major oil and natural gas basin during that timespan.

EPA data released this year also show that oil and natural gas system methane emissions have declined 19 percent since 1990 at the same time natural gas production has increased 51 percent and oil production has increased 28 percent.

The IEA’s latest World Energy Outlook (WEO) also confirms that the U.S. oil and gas industry is outpacing the rest of the world when it comes to methane mitigation, with leakage rates 30 percent below the global average of 1.7 percent. The WEO also confirms that natural gas has considerable climate benefits when compared to other traditional fuels, “even taking methane leakage into account.”

The latest EPA data also show emissions of criteria pollutants responsible for killing millions worldwide continued to plummet in 2017 thanks to increased natural gas use made possible by fracking.

4. Pipeline Progress (Finally!)

Critical midstream development lagged behind surging upstream development for much of 2017, due largely to the Federal Energy Regulatory Commission’s (FERC) lack of a quorum for more than a half year. But fortunately, FERC finally reached quorum in August and has begun to address a $50 billion backlog of needed pipeline construction projects.

Since August, FERC has approved dozens of natural gas pipeline projects totaling 8 Bcf/d of transportation capacity, including the Atlantic Coast (1.7 Bcf/d) and Mountain Valley (2 Bcf/d) pipeline projects. Earlier in the year, FERC managed to approve the Atlantic Sunrise (1.7 Bcf/d) and Rover (3.25 Bcf/d) pipelines. Both are currently under construction, as are the Leach Express (1.5 Bcf/d), Nexus (1.5 Bcf/d) and Mariner East 2 pipelines.

On the oil side, the Dakota Access Pipeline (DAPL) is finally in operation following a well-publicized “Keep It In the Ground”-generated saga, and the DAPL is already spearheading Bakken resurgence. The Keystone XL has also finally cleared its final regulatory hurdle nine years after sparking the anti-pipeline madness that the “Keep It In the Ground” movement continues to cling to, knowing full and well that impeding pipeline construction is its only potential path to achieving its stated goal of curtailing U.S. oil and gas development.

That said, despite some welcome pipeline progress in 2017, the latter KIITG focus will no doubt remain an obstacle moving forward. As acting FERC Chairman Neil Chatterjee recently said,

“e see well funded, sophisticated national environmental organizations that understand how to use all the levers of state and federal government to frustrate pipeline development.”

Speaking of state government, New York officials continues to block several key projects (Constitution, Valley Lateral, Millenium, Northern Access) despite having a state energy plan that calls for the use of more natural gas.

Nonetheless, the midstream bottleneck that impeded the shale revolution from reaching its full potential — particularly in the Appalachian Basin, where $23 billion has been invested in various projects — is finally widening a bit.

5. U.S. Upstream Investment Skyrockets

A recent report finds the U.S. is the most attractive region for upstream oil and gas investment. That could explain why the IEA’s 2017 World Energy Investment report finds that U.S. shale investment grew 53 percent in 2017, far outpacing upstream oil and gas investment in other countries.

Major investments announced this year include ExxonMobil’s acquisition of roughly 275,000 acres in the Permian Basin for $6.6 billion in January, as well as EQT’s $8.2 billion acquisition of Marcellus producer Rice Energy.

Overall, there was $19.8 billion in private equity funding raised for energy ventures in the first quarter of the year alone. This focus in investment shows no signs of slowing either, as oil producers are expected to spend $100 billion in U.S. oil fields next year.

6. Petrochemical Manufacturing Booming — Thanks to Shale

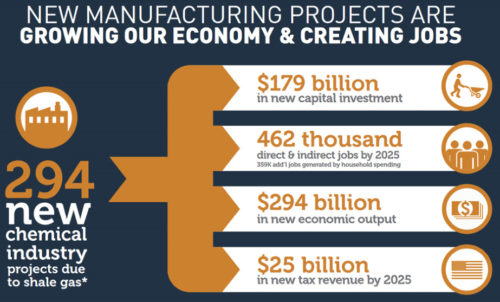

The American Chemistry Council (ACC) reported earlier this year that 310 chemical industry projects totaling $185 billion in new capital investment are currently in the works. These projects are expected to create 464,000 direct or indirect jobs by 2025, and all of this is happening for one reason — the shale gas revolution.

ACC’s announcement actually came before news broke in November that China Energy Investment Corp. plans to invest $83.7 billion in shale-related chemical manufacturing, power generation and underground LNG storage facilities in West Virginia.

That is just one of the exciting major announcements made in Appalachia this year, as a pair of ethane cracker facilities are in the works in Ohio and Pennsylvania, respectively, as is a possible major storage hub for NGLs used for plastics manufacturing.

The Gulf coast is also home to eight of the nine new ethylene cracker plant facilities recently built or under construction in the U.S., as well as three expansion projects and the only facility in America that is being re-started.

No wonder plastics manufacturing is suddenly booming, as it manufacturing in general. A recent report found U.S. manufacturing output is at a 13-year high.

None of this investment, whether in the Gulf Coast or Appalachia, would be possible without fracking unlocking the vast needed resources to rejuvenate American manufacturing. As Mark Denzler, Vice President & Chief Operating Officer of the Illinois Manufacturers’ Association, told EID in the fall,

“According to recent studies, nearly 90 percent of manufacturers are optimistic about the economy and data shows that factory orders are at a 13-year high. Innovative energy production, especially in shale with hydraulic fracturing, are helping lead this renaissance economy by creating low cost and efficient sources of energy. As the primary feedstock, it is also leading to a resurgence in the American chemical industry.”

6. Shale Continues to Bolster America’s Global Standing

It wasn’t that long ago that the robust energy might of other nations — usually ones not particularly friendly to the U.S. — was used to manipulate America’s geopolitical influence and compromise our global standing. But thanks to fracking, that is no longer the case.

Whether it be the current turmoil in the Middle East or crisis in Venezuela, chaos in other parts of the world now has virtually no adverse affect on American energy prices and supply, and therefore isn’t forcing the U.S. to take a compromised position on the world stage.

As New York Times columnist Bret Stephens recently wrote,

“Fracking has meant we could sanction Iran’s oil exports and barely feel the consequences at the pump. … It turns out that we are in an era of energy superabundance, in which the United States is again the global leader.”

The United States’ renewed geopolitical might could very well be encapsulated by the recent five-year deal it struck to deliver LNG to Poland. Like much of the European Union — which has relied on Russia for 40 percent of its oil and 66 percent of its natural gas in recent years — Poland has long been under Vladimir Putin’s thumb. But America’s foray into the European energy market could ultimately erode Russia’s long-held status as a bully in the region.

As Jason Bordoff, director of the Center on Global Energy Policy at Columbia University and a former energy official in the Obama administration, recently said,

“The arrival of the U.S. gas is making Russia nervous. And they should be nervous.”

“Forcing Russia to compete in a more competitive gas market in Europe and giving European consumers alternative sources of supply significantly weakens Russia’s geopolitical influence in Europe. The transition of the U.S. to one of the world’s largest gas exporters has very significant economic, environmental and geopolitical implications.”

That said, it really should come to no surprise that U.S. intelligence officials have confirmed long-held suspicions that Russia has pushed anti-fracking propaganda in an effort to undermine the industry (and also, possibly, funded U.S. green groups that oppose fracking). But oddly enough, despite being obsessed with Russia’s meddling in the U.S. election, the media has continued to largely ignore the Kremlin’s increasingly evident efforts to undermine America’s oil and natural gas industry.

8. Regulatory Rollback

Another major contributor to the oil and natural gas industry’s resurgence in 2017 was the refreshing new environment of regulatory sanity at the federal level.

The Trump administration announced on Thursday that it will repeal the Obama-era Bureau of Land Management (BLM) fracking rule in January, officially disposing of duplicative regulations that are already being enforced at the state level.

The BLM venting and flaring rule has also officially been suspended until 2019 and will likely never see the light of day in its current costly and duplicative form (even though environmentalists continue to fight the rule’s suspension in court).

The EPA also announced in June its intent to delay for two years the Obama administration’s New Source Performance Standards (NSPS) targeting methane in order to reconsider certain aspects of the rule. Though the courts have rejected the EPA’s delay and the rule is currently in effect, Congress has voted not to fund the rule, and its future remains bleak.

By rolling back these costly, duplicative and unnecessary regulations, the current administration has allowed the oil and natural gas industry to drive U.S. employment and GDP growth in 2017. Not coincidentally, the U.S. economy grew three percent in the third quarter. And oh by the way, oil and gas methane emissions have continued to decline without these rules, and the U.S. has continued to enjoy the previously unheard of coupling of declining greenhouse gas emissions and economic growth.

9. Health Research Confirms Fracking is Protective of Public Health

Several new studies were released this year showing that fracking is protective of public health. And unlike a vast majority of the research that has reached the opposite inclusion, these studies were based on actual measurements.

In February, the Colorado Department of Public Health released a health assessment based on 10,000 air samples taken near oil and gas development that concluded,

“he risk of harmful health effects is low for residents living oil and gas operations,” and that “results from exposure and health effect studies do not indicate the need for immediate public health action.”

In the spring, a pair of peer-reviewed studies — one conducted by the United States Geological Survey (USGS) and the other partially funded by the anti-fracking Natural Resources Defense Council — added to the overwhelming evidence that fracking is not a major threat to drinking water.

And in December, a comprehensive evaluation of Pennsylvania Department of Health data found that mortality rates in six most heavily drilled Pennsylvania counties have declined or remained stable since shale production began in the region. The report also found unconventional gas development was not associated with an increase in infant mortality in the top Marcellus counties, noting that

“the mortality rate significantly declined (improved), even surpassing the improvement of the state.”

Frankly, the collective findings of these studies should merit a higher ranking on our year-end list. But unfortunately, they received relatively little media coverage when compared to studies such as a recent widely covered report linking fracking to low birth weight. That study — similar to many before it — claimed to find causal evidence of fracking’s health harms despite failing to take direct measurements. It also failed to control for known causes of infant health problems (smoking, alcohol use and drug use) and included contradictory data that the authors (and media) simply ignored or glossed over.

10. “Keep It in The Ground” Movement Gets More Desperate and Extreme

With all the good shale-related news that came out in 2017, it shouldn’t come as a surprise that the “Keep It In the Ground” movement stepped up its extreme tactics in 2017, with some of its antics ranging from desperate to downright scary.

Here are just a few of the most extreme headlines, along with details on the most desperate and extreme KIITG antics this year.

- In March, an Ohio anti-fracking group organizer who has been involved in repeated failed efforts to pass a local fracking ban in Youngstown pled guilty to 13 felony counts for false voter registration and election fraud. She was even found guilty of registering deceased people to vote. Apparently she didn’t find enough, as the Youngstown fracking ban failed for the sixth straight time this year.

- In April, a Colorado activist suggested blowing up wells and “eliminating fracking workers” in a letter to the editor. Even worse, the activist actually stood by the comment days later, telling Colorado Politics, “I wouldn’t have a problem with a sniper shooting one of the workers” at a well site, “I believe fracking is murder.”

- In October, less than two days after the deadliest mass shooting in modern U.S. history, Boulder, Colo., protesters staged what they called a “die-in” against fracking. To make matters worse, the tasteless stunt doubled as a fundraiser for the groups involved.

- In September, the Associated Press reported that Michigan State University professor Elizabeth LaPennsee created a video game in which, “Players can earn points by firing lightning at snakelike pipelines, trucks and other oil industry structures.” LaPennsee defended her “work” by explaining that players have the option to bring people and animals back to life, and also claimed the game was not intended to incite violence against energy workers.

- In December, the Long Beach Press Telegram reported that a consultant attending a meeting to advocate for a proposed drilling plan was attacked following the meeting “by someone who opposed the plan, according to accounts from a witness and authorities.”

- Also in December, the Olympia Spokesman-Review reported that a protest in which activists and anarchists blocked a railway used to ship fracking supplies cost the city roughly $40,000. The paper also reported that the 15 tons of debris hauled away from the protest site included knives, sharpened pieces of metal and used syringes.

- Also in December, Canadian KIITG activists claimed they vandalized the home and damaged cars of a Quebec oil and gas industry executive.

- Also in December, The Bismarck Tribune reported that six police officers testified that a pipeline protester said, “If I wanted to kill you, I would have shot you in the head” and “All pigs deserve to die,” while laughing after being arrested at a Dakota Access Pipeline protest.

The “Keep It In the Ground” movement continues to insist that it is not an extreme movement. The headlines generated in December alone refute that claim emphatically.

Conclusion

The past year was unquestionably a positive one for the U.S. oil and natural gas industry, and all signs point to 2018 being even better. Not only has hydraulic fracturing unlocked our country’s enormous energy potential, the current regulatory and global environment has the U.S. positioned to achieve “energy dominance” that will not only continue to strengthen our own economy and allow to further reduce emissions, but allow the rest of the world to do so as well.

These are truly exciting times. But as our final two top storylines of 2017 remind us, increasingly extreme “Keep It In the Ground” misinformation and tactics will remain key challenges moving forward.

From everyone at Energy In Depth, have a safe and happy New Year!

Source: Daily Dose of ShaleDirectories.com NewsThursday, December 28, 2017

IPAA, Western Energy Alliance Applaud Repeal Of Hydraulic Fracturing Rule

Wednesday, December 27, 2017

Chinese Ships Reportedly Spotted Transferring Oil To North Korea

U.S. reconnaissance photos reportedly show Chinese vessels trading oil products with North Korean ships, a violation of UN sanctions. Diplomats from an Asian country confirmed information published this week in the South Korean press that such trade persists despite sanctions, according to The Financial Times.

Source: Daily Dose of ShaleDirectories.com News

Source: Daily Dose of ShaleDirectories.com News

Tuesday, December 26, 2017

Explosion Hits Pipeline Feeding Libya's Es Sider Terminal

Thursday, December 21, 2017

Year in Review: 2017 Was a Stellar Year for Oil and Gas

With the new year fast approaching, millions of Americans are turning to oil and natural gas to make their holiday festivities possible. From the natural gas heating our homes, to the fuel in cars and planes helping us reach family and friends across the country, to numerous petroleum-based gifts we’ll be exchanging this Christmas, oil and natural gas play an integral part of our holidays whether we realize it or not.

To celebrate everything oil and gas provides this time of year, let’s look back and appreciate the most remarkable shale-related trends that have occurred in 2017.

Soaring Production

Despite activists best (and strangest) efforts, American oil and natural gas production soared in 2017. Already the world’s largest oil and natural gas producer since 2012, U.S. oil production grew by over 650,000 barrels per day (b/d) between January and September of this year. Even more impressive, U.S. oil production is projected to keep growing into 2018, with the U.S. Energy Information Administration estimating an additional 94,000 b/d increase in January of next year. Still not enough? The agency forecasts U.S. crude output will reach over 10 million b/d – a new record – thanks to a nearly 1.2 million b/d increase in oil production from shale development alone in 2017.

Through shale development, U.S. natural gas production has grown as well. Between January and December of this year, U.S. shale gas output grew from about 47.6 billion cubic feet per day (Bcf/d) to over 62.2 Bcf/d – a near 31 percent increase. Natural gas output from shale is projected to grow even further, with EIA estimating an increase of 764 million cubic feet per day (Mcf/d) from December 2017 to January 2018, with almost half of that production stemming from the Appalachia region alone.

Declining Emissions

Considering the incredible oil and natural gas production growth seen this year, the strides oil and gas producers are making on mitigating emissions levels are that much more impressive. A new report from Energy in Depth found methane emissions across eight of the country’s largest oil and gas producing regions have declined by over 10.8 million metric tons (MMT) of CO2 equivalent from 2011 to 2016. In some of the most prolific shale basins, such as West Texas’ Permian, this means that while production has roughly doubled over that period, emissions declined – by 6.3 percent in the Permian’s case, or an amazing 47 percent in New Mexico’s San Juan basin.

This report caps off a year of stellar news about emissions reductions from oil and gas development. Earlier this year, EIA found that sulfur dioxide emissions (SO2) produced from U.S. power generation declined 73 percent from 2003 to 2015 as natural gas has become increasingly relied on for electricity in the United States. Along the same lines, EIA also published data this year showing that 63 percent of the 89 MMT drop in CO2 emissions in 2016 could be directly attributed to switching to natural gas for electricity generation. Overall, shifting to natural gas for power production has resulted in a 2,007 MMT reduction in CO2 emissions since 2005, almost twice the amount that can be attributed to renewable energy sources.

More recently, research has found that emissions mitigation techniques are continuing to improve. As a September report from Bloomberg New Energy Finance found, efforts by the five largest oil and natural gas companies resulted in an average 13 percent decline in greenhouse gas emissions between 2010 and 2015, with companies like Exxon and BP reducing emission by 14 percent and 25.5 percent, respectively. Further, a November study from Penn State and funded by the U.S. Department of Energy found methane leakage rates from natural gas activities in the Northeast Marcellus Shale accounted for just 0.4 percent of production. This is well below the rate at which experts estimate emissions would negate the climate benefits of natural gas use – about 2.0 percent – as well as the current estimated global leakage rate of 1.7 percent.

Remarkably, the U.S. has led the world in CO2 reductions since 2005 at the same time that it emerged as the world’s top oil and gas producer. We have done this while experiencing significant economic growth — a previously unheard of decoupling trend — and also reducing oil and natural gas system methane emissions by two percent.

Growing Exports

With production skyrocketing and emissions dropping thanks to increased natural gas use, the United States is now in a unique position to help trading partners around the globe achieve their climate goals through liquefied natural gas (LNG) exports. With only one terminal currently in operation and the first shipment of U.S. LNG taking place less than two years ago, American LNG exports have flourished over the past year.

According to EIA, U.S. LNG exports averaged 1.9 Bcf/d through November of this year, something almost unthinkable 10 years ago when the U.S. was importing over 3 Bcf of LNG per day. Moreover, U.S. LNG export capacity increased from about 1.5 Bcf/d in January to roughly 2.8 Bcf/d, with capacity expected to nearly quadruple by 2019 as additional terminals come on line.

Coupled with increased natural gas pipeline exports and decreased reliance on imported natural gas, this year also saw the United States becoming a net exporter of natural gas for the first time in nearly 60 years.

But natural gas wasn’t alone in its export growth over 2017, as oil exports hits record highs as well. In November, U.S. crude exports to China hit an all-time high of nearly 290,000 b/d, with overall U.S. crude exports to Asia hitting a record 877,000 b/d and challenging the OPEC countries as top suppliers to key Asian importers. Considering the ban on U.S. oil exports was lifted just two years ago, America’s improving position as a key player in the global oil market is that much more astonishing.

Billions of Dollars in Investment

Unsurprisingly, the growth in production and exports has been met with equal enthusiasm for increased investment in shale development. According to the International Energy Agency (IEA) 2017 World Energy Investment report, U.S. shale investment grew 53 percent in 2017, with the next largest increase in spending coming from Russia at only six percent.

This growth in investment was apparent right off the bat, with ExxonMobil acquiring roughly 275,000 acres in the Permian for $6.6 billion in January, while other major news this year included EQT’s $8.2 billion acquisition of Marcellus producer Rice Energy and the $19.8 billion in private equity funding raised for energy ventures in the first quarter of the year alone. This focus in investment shows no signs of slowing either, as oil producers are expected to spend $100 billion in U.S. oil fields next year.

Upstream isn’t the only segment of the industry that saw a surge in investment this year, however. As a key component in the manufacture of chemicals, the growth in U.S. shale production has so far spurred $185 billion in chemical project capital investment, according to the American Chemistry Council. Additionally, production from the Eagle Ford shale is driving $50 billion in port and export infrastructure investment at the Port of Corpus Christi alone.

Conclusion

There are so many benefits from oil and gas for which to be thankful this year; from record production dropping prices for consumers, to billions of dollars in investment providing new jobs and economic growth. But if nothing else, 2017 showed the oil and gas industry is strong and here to stay.

Hope you have a safe Holiday Season and happy New Year!

Source: Daily Dose of ShaleDirectories.com Newshttps://www.shaledirectories.com/blog/year-in-review-2017-was-a-stellar-year-for-oil-and-gas/

Appalachian Producers Share Forecasts at 2018 Marcellus-Utica MIDSTREAM Conference

FOR IMMEDIATE RELEASE

Contact: Kate Clark

713.260.4657

Appalachian Producers Share Forecasts at 2018 Marcellus-Utica MIDSTREAM Conference

HOUSTON (December 7, 2017) – As the nation’s second LNG export facility starts running in 2018, Appalachian operators will gather in Pittsburgh, PA for the Marcellus-Utica MIDSTREAM conference and exhibition January 30 – February 1, 2018. Companies like Dominion Energy, Crestwood Equity Partners, Antero Resources and more will join 1,000+ industry professionals for the two-day event at the David L. Lawrence Convention Center. “Cove Point’s LNG terminal opening will draw operators’ attention to the Marcellus and Utica,” said Chris Sheehan, Senior Financial Analyst for Oil and Gas Investor. “The keynote presentations at this year’s Marcellus-Utica MIDSTREAM conference give insights to takeaway capacity and forward-looking strategies, offering valuable market intelligence to all who attend.” The two-day event will feature the latest production forecasts, plus updates on emerging Appalachian markets and the regions’ expanding takeaway capacity. In the Wednesday morning keynote, Crestwood Equity Partners’ CEO Robert (Bob) G. Phillips will compare and contrast supply dynamics and infrastructure across the regions’ two plays. Phillips will share his company’s predictions of pending opportunities opening up in 2018 and beyond. During Thursday’s Opening Keynote, Dominion Energy’s Senior Vice President Donald R. Raikes will discuss the Cove Point LNG export facility poised to begin shipments in early 2018. Dominion’s LNG terminal launch marks the debut of an east coast outlet for U.S. gas exports to markets across the Atlantic and beyond. Raikes and Phillips will be joined by other executives who will lead keynote presentations, panels, company spotlights and more. Other featured speakers include:- Matthew Hite, Vice President of Government Affairs, GPA Midstream Association

- Chris Akers, President & Chief Operating Officer, Eureka Midstream

- Kyle Mork, CEO, GreyRock Energy

- Dana Bryant, Senior Vice President, Midstream & Marketing, Eclipse Resources

- Robert F. Powelson, Commissioner, Federal Energy Regulatory Commission

- Steven M. Woodward, Senior Vice President – Business Development, Antero Resources Corp./ Antero Midstream Partners LP

- Erin Petkovich, Director, Northeast Business Development, Enbridge

About Hart Energy

For more than 40 years, Hart Energy editors and experts have delivered market-leading insights to investors and energy industry professionals. The Houston-based company produces award-winning magazines (such as Oil and Gas Investor, E&P and Midstream Business); online news and data services; in-depth industry conferences (like the DUG™ series); GIS data sets and mapping solutions; and a range of research and consulting services. For information, visit hartenergy.com.Winter weather predictions by the Farmer’s Almanac, La Nina effect and Natural Gas Price

When looking for weather conditions for the approaching winter I usually to look to the Farmer’s Almanac. The Almanac is usually 80% accurate even with predictions made 18 months in advance. Currently, we have been and will continue to be effected by La Nina, the flipside to El Nino. Being ever vigilant to the day to day weather, working in the oil & gas industry plus being a financial junkie, over the last 18-24 mos it appears the natural gas price is generally another predictor of the weather 60-90 days out. At least it has been. However, wanting to get a holistic predication looked to ole reliable Farmer’s Almanac for their prediction which is:

Farmer’s Almanac -Mid Atlantic and OH Valley Region forecast

NOVEMBER 2017: temperature 45° (2° below avg.); precipitation 8.5" (5" above avg.); Nov 1-3: Rainy, mild; Nov 4-6: Sunny, cool; Nov 7-11: Heavy rain, then sunny, cool; Nov 12-18: Rain, then sunny, chilly; Nov 19-24: Rainy periods, cool; Nov 25-30: Rain and wet snow north; sunny, mild south.

DECEMBER 2017: temperature 42° (1° above avg. north, 5° above south); precipitation 4" (1" above avg.); Dec 1-4: Rainy, mild; Dec 5-11: Rain, then sunny, cold; Dec 12-20: Rainy periods, mild; Dec 21-23: Sunny, cold; Dec 24-27: Rainy, mild; Dec 28-31: Snow, then sunny, cold.

THEN, to current forecasting for the La Nina effect:

The National Oceanic and Atmospheric Administration said a weak La Nina has formed and is expected to stick around for several months- much longer than last year. La Nina is a natural cooling of parts of the Pacific that alters weather patterns around the globe. La Nina is well known to be a major disruptor of weather patterns. Because La Nina shifts storm tracks, it often brings more snow in the Ohio and Tennessee Valleys. Typically the snowfall is generally slightly above average snowfall. However, the New England states are often recipients of more snow.

Speaking of the New England region they may be hampered by colder and heavier snowfall than the Appalachian region however, this region has little effect on natural gas prices. The New England states get their natural gas from foreign ships that sit on their coastline and transports natural gas from foreign counties via pipeline which is much more costly. I guess they’d rather buy the foreign natural gas than support pipelines to bring the Marcellus gas at a lower cost.

As for the commodity price of nat gas, short term it appears to decrease with a slight increase early 2018.

Nat Gas prices down 30% ytd; nat gas inventories down 182 Billion cubic feet from last year (as reported by CNBC 12.21.17). The nat gas price seems to align with both Farmer’s Almanac and the La Nina effect – for now. However, with aggressive efforts to bring pipelines on line, exports of nat gas increasing and nat gas powered electric grids coming on line; this may be the last year the price of nat gas could be viewed as a predictor of the weather. Stay tuned, 2018 will be a rock n’ roll year for natural gas emerging opportunities.

Joseph Barone

President

Shale Directories, LLC

www.shaledirectories.com

jbarone@shaledirectories.com

Hydraulic Fracking Credited for decline in Methane Gas

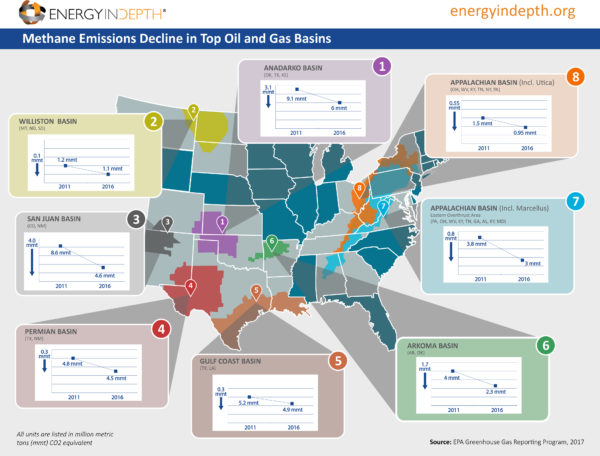

A new Energy in Depth report (thank you Seth) shows that methane emissions from oil and natural gas development nationally continues to decline in the top basins across the United States. This decline is real even as oil and gas production continues to increase.

Based on the latest data from the U.S. Environmental Protection Agency’s (EPA) Greenhouse Gas Reporting Program, EID’s report shows methane emissions from the most productive shale basins in the country have fallen considerably in the past six years. These reductions have been achieved even as oil and natural gas production has increased 54 percent and 16 percent, respectively, during that time thanks to advances in horizontal drilling and hydraulic fracturing technology.

In the Appalachian Basin — which includes the surging Marcellus and Utica shales — methane emissions have fallen 26 percent since 2011 at the same time natural gas production in the region has more than quadrupled, as the following Energy Information Administration (EIA) graphic illustrates.

Based on the latest data from the U.S. Environmental Protection Agency’s (EPA) Greenhouse Gas Reporting Program, EID’s report shows methane emissions from the most productive shale basins in the country have fallen considerably in the past six years. These reductions have been achieved even as oil and natural gas production has increased 54 percent and 16 percent, respectively, during that time thanks to advances in horizontal drilling and hydraulic fracturing technology.

In the Appalachian Basin — which includes the surging Marcellus and Utica shales — methane emissions have fallen 26 percent since 2011 at the same time natural gas production in the region has more than quadrupled, as the following Energy Information Administration (EIA) graphic illustrates.

The EIA recently noted the Appalachian Basin has increased natural gas production by 14 billion cubic feet per day (Bcf/d) since 2012, growing from 7.8 Bcf/d in 2012 to an incredible 23.8 Bcf/d in 2017.

Speaking of surging production, the Permian Basin, has experienced such a historical production increase in recent years that the term “Permania” has been coined to describe the boom currently underway in west Texas and New Mexico, which is illustrated in the following EIA graphics.

The EIA recently noted the Appalachian Basin has increased natural gas production by 14 billion cubic feet per day (Bcf/d) since 2012, growing from 7.8 Bcf/d in 2012 to an incredible 23.8 Bcf/d in 2017.

Speaking of surging production, the Permian Basin, has experienced such a historical production increase in recent years that the term “Permania” has been coined to describe the boom currently underway in west Texas and New Mexico, which is illustrated in the following EIA graphics.

Despite the fact that production in the Permian doubled from 2011 to 2016, methane emissions have decreased 6.3 percent, according to GHGRP data. Coupled with a 5.8 percent reduction in methane emissions in the Gulf Coast Basin since 2011, EPA data confirms that the country’s top oil- and gas-producing state is also a leader in methane emission reductions.

EPA data also show that methane emissions in the Williston Basin — home of the Bakken Shale in North Dakota and Montana — have fallen 8.3 percent from 2011 to 2016. These declines came at the same time that oil and natural gas production in the region has quadrupled, as the following EIA graphics show.

Despite the fact that production in the Permian doubled from 2011 to 2016, methane emissions have decreased 6.3 percent, according to GHGRP data. Coupled with a 5.8 percent reduction in methane emissions in the Gulf Coast Basin since 2011, EPA data confirms that the country’s top oil- and gas-producing state is also a leader in methane emission reductions.

EPA data also show that methane emissions in the Williston Basin — home of the Bakken Shale in North Dakota and Montana — have fallen 8.3 percent from 2011 to 2016. These declines came at the same time that oil and natural gas production in the region has quadrupled, as the following EIA graphics show.

Similarly, the Anadarko has emerged as one of the fastest growing oil and natural gas basins in recent years. But despite being one of the fastest growing basins in the country, methane emissions in the Anadarko Basin have decreased 34 percent since 2011 at the same time production has reached new heights.

Similarly, the Anadarko has emerged as one of the fastest growing oil and natural gas basins in recent years. But despite being one of the fastest growing basins in the country, methane emissions in the Anadarko Basin have decreased 34 percent since 2011 at the same time production has reached new heights.

Even in the San Juan Basin — long a focal point of the “Keep It In The Ground” movement’s push for methane regulations, due to the presence of a methane “hot spot” above the Four Corners region of the basin — methane emissions have fallen by 47 percent since 2011, as the following EID graphic illustrates.

Even in the San Juan Basin — long a focal point of the “Keep It In The Ground” movement’s push for methane regulations, due to the presence of a methane “hot spot” above the Four Corners region of the basin — methane emissions have fallen by 47 percent since 2011, as the following EID graphic illustrates.

Overall, EPA data show methane emissions from major onshore oil and natural gas production facilities declined by nearly 14 million metric tons between 2011 and 2016.

As “Keep It In the Ground” groups continue to push the EPA and BLM methane rules — claiming that voluntary efforts such as the initiative recently announced by the American Petroleum Institute don’t work — this data show that the exact opposite is true. As the EPA observed in 2014:

“The decrease in production emissions is due to increased voluntary reductions, from activities such as replacing high bleed pneumatic devices, regulatory reductions, and the increased use of plunger lifts for liquids unloading.”

This report should clearly discredit a Dec 15, 2017 report of health risks to babies born near fracking sites. That report lacks any medical or clinical statistics.

Joseph Barone

President

Shale Directories, LLC

www.shaledirectories.com

jbarone@shaledirectories.com

Overall, EPA data show methane emissions from major onshore oil and natural gas production facilities declined by nearly 14 million metric tons between 2011 and 2016.

As “Keep It In the Ground” groups continue to push the EPA and BLM methane rules — claiming that voluntary efforts such as the initiative recently announced by the American Petroleum Institute don’t work — this data show that the exact opposite is true. As the EPA observed in 2014:

“The decrease in production emissions is due to increased voluntary reductions, from activities such as replacing high bleed pneumatic devices, regulatory reductions, and the increased use of plunger lifts for liquids unloading.”

This report should clearly discredit a Dec 15, 2017 report of health risks to babies born near fracking sites. That report lacks any medical or clinical statistics.

Joseph Barone

President

Shale Directories, LLC

www.shaledirectories.com

jbarone@shaledirectories.com

Based on the latest data from the U.S. Environmental Protection Agency’s (EPA) Greenhouse Gas Reporting Program, EID’s report shows methane emissions from the most productive shale basins in the country have fallen considerably in the past six years. These reductions have been achieved even as oil and natural gas production has increased 54 percent and 16 percent, respectively, during that time thanks to advances in horizontal drilling and hydraulic fracturing technology.

In the Appalachian Basin — which includes the surging Marcellus and Utica shales — methane emissions have fallen 26 percent since 2011 at the same time natural gas production in the region has more than quadrupled, as the following Energy Information Administration (EIA) graphic illustrates.

The EIA recently noted the Appalachian Basin has increased natural gas production by 14 billion cubic feet per day (Bcf/d) since 2012, growing from 7.8 Bcf/d in 2012 to an incredible 23.8 Bcf/d in 2017.

Speaking of surging production, the Permian Basin, has experienced such a historical production increase in recent years that the term “Permania” has been coined to describe the boom currently underway in west Texas and New Mexico, which is illustrated in the following EIA graphics.

Despite the fact that production in the Permian doubled from 2011 to 2016, methane emissions have decreased 6.3 percent, according to GHGRP data. Coupled with a 5.8 percent reduction in methane emissions in the Gulf Coast Basin since 2011, EPA data confirms that the country’s top oil- and gas-producing state is also a leader in methane emission reductions.

EPA data also show that methane emissions in the Williston Basin — home of the Bakken Shale in North Dakota and Montana — have fallen 8.3 percent from 2011 to 2016. These declines came at the same time that oil and natural gas production in the region has quadrupled, as the following EIA graphics show.

Similarly, the Anadarko has emerged as one of the fastest growing oil and natural gas basins in recent years. But despite being one of the fastest growing basins in the country, methane emissions in the Anadarko Basin have decreased 34 percent since 2011 at the same time production has reached new heights.

Even in the San Juan Basin — long a focal point of the “Keep It In The Ground” movement’s push for methane regulations, due to the presence of a methane “hot spot” above the Four Corners region of the basin — methane emissions have fallen by 47 percent since 2011, as the following EID graphic illustrates.

Overall, EPA data show methane emissions from major onshore oil and natural gas production facilities declined by nearly 14 million metric tons between 2011 and 2016.

As “Keep It In the Ground” groups continue to push the EPA and BLM methane rules — claiming that voluntary efforts such as the initiative recently announced by the American Petroleum Institute don’t work — this data show that the exact opposite is true. As the EPA observed in 2014:

“The decrease in production emissions is due to increased voluntary reductions, from activities such as replacing high bleed pneumatic devices, regulatory reductions, and the increased use of plunger lifts for liquids unloading.”

This report should clearly discredit a Dec 15, 2017 report of health risks to babies born near fracking sites. That report lacks any medical or clinical statistics.

Joseph Barone

President

Shale Directories, LLC

www.shaledirectories.com

jbarone@shaledirectories.com

Wednesday, December 20, 2017

Fight Over Alaska Arctic Drilling Has Just Begun, Opponents Vow

U.S. Senator Lisa Murkowski, an Alaska Republican, won a decades-long battle Dec. 20 to open part of an Arctic wildlife reserve in her state to oil and gas drilling, but Democratic senators and conservationists vow the war has only begun.

The tax bill passed by Congress contains language pushed by Murkowski and supported by President Donald Trump to hold two lease sales in the 1.5 million-acre 1002 area on the northern coastal plain of the Arctic National Wildlife Refuge (ANWR).

Democrats and environmentalists deplore the prospect of development in ANWR, home to polar and grizzly bears, 200 species of birds, and where Gwich’in natives depend on migrating herds of porcupine caribou.

Source: Daily Dose of ShaleDirectories.com News

Source: Daily Dose of ShaleDirectories.com News

Tuesday, December 19, 2017

Linn Energy To Sell Oklahoma Waterflood, Texas Panhandle Assets For $122 Million

Linn Energy Inc. (OTC: LNGG) said Dec. 19 it will close out an already blockbuster 2017 of A&D activity with yet another asset sale as it continues the transformation it embarked on earlier this year.

The Houston-based company agreed to sell its Oklahoma waterflood and Texas Panhandle properties to an undisclosed buyer for $122 million. Combined the assets cover roughly 179,000 net acres with net production of about 5,200 barrels of oil equivalent per day (boe/d) for third-quarter 2017.

Since exiting bankruptcy reorganization in February 2017, Linn has focused on transforming itself from an MLP with assets scattered across the Lower 48 to a streamlined, growth-oriented E&P. As a result, the company has divested or agreed to sell more than $1.6 billion in noncore assets so far this year.

Source: Daily Dose of ShaleDirectories.com News

Source: Daily Dose of ShaleDirectories.com News

Monday, December 18, 2017

McDermott and CB&I Agree To Combine In $6 Billion transaction

Upon completion of the transaction, McDermott shareholders will own approximately 53% of the combined company on a fully diluted basis and CB&I shareholders will own approximately 47%, according to the a press release. Under the terms of the business combination agreement (BCA), CB&I shareholders will be entitled to receive 2.47221 shares of McDermott common stock for each share of CB&I common stock owned (or 0.82407 shares if McDermott effects a planned three-to-one reverse stock split prior to closing), subject to any withholding taxes. The estimated enterprise value of the transaction is approximately $6 billion, based on the closing share price of McDermott on Dec. 15.

Source: Daily Dose of ShaleDirectories.com News

Source: Daily Dose of ShaleDirectories.com News

Friday, December 15, 2017

Noble, CNX Settle Legal Dispute With Marcellus Midstream Sale

In hopes of continuing its planned Appalachia exit, Noble Energy Inc. (NYSE: NBL) reached an agreement on Dec. 15 with CNX Resources Corp. (NYSE: CNX) to sell its Marcellus midstream assets, quickly resolving a lingering legal dispute between the two companies.

In the agreement, CNX Resources will acquire Noble’s 50% interest in CONE Gathering LLC, which owns the general partner of CONE Midstream Partners LP (NYSE: CNNX), for $305 million cash. Noble will retain its 21.7 million common limited partner units in CONE Midstream with plans to divest them over the next few years, according to a company press release.

As a result of the transaction with CNX, Noble terminated its prior agreement to divest its entire Marcellus midstream holdings to Wheeling Creek Midstream LLC, a portfolio company of Quantum Energy Partners, for $765 million. That particular deal came under fire when CNX, which holds a 50% interest in CONE Gathering, filed a suit to enjoin Noble’s transaction with Wheeling Creek.

Source: Daily Dose of ShaleDirectories.com News

Source: Daily Dose of ShaleDirectories.com News

https://www.shaledirectories.com/blog/noble-cnx-settle-legal-dispute-with-marcellus-midstream-sale/

Monday, December 11, 2017

TorcUP Introduces the VOLTA Battery

The VOLTA Battery-Powered Torque Wrench is the newest addition to TorcUP, Inc.’s extensive line of industrial bolting tools. Power-driven by a Lithium Ion 6.2 Ah re-chargeable battery, the VOLTA combines cutting-edge technology with the freedom and flexibility of cordless operation making it ideal for the oil and gas industry.

The VOLTA’s precision-engineered, brushless motor delivers efficiency, longer run-time and extended durability, while its configurable torque range capabilities ensure ease of use and repeatability. The tool’s internal brushless technology also allows the wrench to run cooler, providing bolting application safety and versatility in harsh environments like well sites and pipelines in the Marcellus and Utica shale plays as well as shale plays in Texas, North Dakota and Colorado.

Additional features include digital display, torque memory settings, automatic reaction arm release and ft/lb to Nm conversion. The VOLTA is available in two drive sizes (3/4” and 1”) and four models with a torque ranges from 120 ft/lbs to 3, 000 ft/lbs.

TorcUP, Inc. has been providing industrial torque and bolting solutions since 1996. We offer worldwide sales, support and service. All of our tools are proudly Made In USA. Visit www.torcup.com to view our full product line.

For more information, contact:

Jessica Wise

TorcUP, Inc.

(610) 250-5800 ext. 124

jessicaw@torcup.com

www.torcup.com

Dissecting the Frasier Institute Report

Fast Facts Intro:

Fast Facts Intro:

- Report ranks 97 international jurisdictions that collectively represent 52 percent of proved oil and gas reserves worldwide and 66 percent of global oil and gas production. The rankings do not take into account the amount of proved reserves in a jurisdiction.

- Completing this report were 333 oil and gas executives and managers responded to this year’s survey, which evaluates jurisdictions based on investment factors

- The investment factors are highly influenced by Policy Perception Indexes (PPL) which include but not limited to fiscal terms, taxation, environmental regulations, regulatory costs, consistency and enforcement, political stability, quality of infrastructure and geology, and availability of a skilled workforce

- Among the 15 jurisdictions with the largest petroleum reserves worldwide, Texas is number one, followed by United Arab Emirates, Alberta(Canada), Kuwait and Egypt.

- Among regions, Venezuela is number one, Europe finished second to the United States, followed by Canada and Australia. Globally, every region except Africa, Canada, Latin America and the Caribbean experienced declines in investment attractiveness, according to the survey.

- This year, U.S. states comprise six of the top 10 jurisdictions around the world:Texas (1st), Oklahoma (2nd ), North Dakota (3rd), West Virginia (5th), Kansas(6 th) and Wyoming (9th).

- California and nine foreign jurisdictions are the least attractive (investment) jurisdictions for oil and gas investments and their PPI rankings reflect it.

Sunday, December 10, 2017

Working gas in storage reverses course, grows

The volume of working natural gas in storage during the week of Dec. 1, increased for the first time in four weeks, signaling the winter storage season isn’t officially underway.

Source: Daily Dose of ShaleDirectories.com News

https://www.shaledirectories.com/blog/working-gas-in-storage-reverses-course-grows/

Saturday, December 9, 2017

H&P's Acquisition Of MagVAR To Bring Shale Drilling Accuracy To New Level

Helmerich & Payne Inc. (NYSE: HP) said Dec. 8 it acquired Magnetic Variation Services LLC (MagVAR), a firm focused on enhancing the accuracy of directional drilling and wellbore optimization.

The Tulsa, Okla.-based company, also known as H&P, didn't disclose the financial terms of the acquisition.

MagVAR was founded in 2010 by Stefan Maus, a senior scientist at the University of Colorado. Through comprehensive 3-D geomagnetic reference modeling, the company provides measurement while drilling (MWD) survey corrections by identifying and quantifying MWD tool measurement errors in real time.

Source: Daily Dose of ShaleDirectories.com News

Source: Daily Dose of ShaleDirectories.com News

Thursday, December 7, 2017

Massachusetts AG Wants Climate Warnings at Gas Stations

In oral arguments Tuesday before a state court, the Massachusetts Attorney General’s chief counsel laid out the state’s case for trying to investigate ExxonMobil for allegedly hiding climate change from consumers. Under heavy questioning from a panel of judges, the AG’s representative repeatedly asserted that ExxonMobil should have included a warning about climate change on all of its advertising – including at the gas pump.

Continue reading on EID Climate.

Source: Daily Dose of ShaleDirectories.com Newshttps://www.shaledirectories.com/blog/massachusetts-ag-wants-climate-warnings-at-gas-stations/

Marketed: Operated Wilcox Properties, Central Louisiana, Petro Harvester

Petro Harvester Oil & Gas LLC is selling certain operated properties in the Central Louisiana Wilcox play through an offering handled by advisory firm TenOaks Energy Advisors LLC.

The offer comprises roughly 7,000 net acres in legacy fields including the Reddell, Pine Prairie, Port Barre, Mamou/Beacon’s Gully, Iberia and Leleux fields. The assets, which have a monthly net cash flow of $1.3 million, are located in Evangeline, St. Landry, Vermilion and Iberia parishes, La.

Source: Daily Dose of ShaleDirectories.com News

Source: Daily Dose of ShaleDirectories.com News

Tuesday, December 5, 2017

DAPL operators to coordinate oil-spill response plan with tribes, Army Corps: judge

Monday, December 4, 2017

Rocky Mountain GTL to build Canadian GTL project

Gas-to-liquids (GTL) technology developer Greyrock Energy said Monday the Rocky Mountain GTL board voted to move forward with construction of a GTL plant roughly 37 miles east of Calgary, near Carseland, Alberta.

Source: Daily Dose of ShaleDirectories.com News

https://www.shaledirectories.com/blog/rocky-mountain-gtl-to-build-canadian-gtl-project/

Friday, December 1, 2017

Trump Plans To Meet Oil Industry Reps On US Biofuel Policy

U.S. President Donald Trump has agreed to meet with representatives of the oil refining industry and their legislative backers to discuss the nation’s biofuels program, according to two sources briefed on the matter.

Source: Daily Dose of ShaleDirectories.com News

Source: Daily Dose of ShaleDirectories.com News

https://www.shaledirectories.com/blog/trump-plans-to-meet-oil-industry-reps-on-us-biofuel-policy/

MIT Challenges EIA’s Oil and NatGas Production Projects

Turns out, America’s decade-long shale boom might just end up being a little too good to be true.

There’s no denying that fracking has turned the U.S. into a force in the global oil and gas markets, which has more than a few people abuzz about the prospect of energy independence.

But now, researchers at MIT have uncovered one potentially game-changing detail: a flaw in the Energy Department’s official forecast, which may vastly overstate oil and gas production in the years to come.

The culprit, they say, lies in the Energy Information Administration’s premise that better technology has been behind nearly all the recent output gains, and will continue to boost production for the foreseeable future. That’s not quite right. Instead, the research suggests increases have been largely due to something more mundane: low energy prices, which led drillers to focus on sweet spots where oil and gas are easiest to extract.

“The EIA is assuming that productivity of individual wells will continue to rise as a result of improvements in technology,” said Justin B. Montgomery, a researcher at the Massachusetts Institute of Technology and one of the study’s authors. “This compounds year after year, like interest, so the further out in the future the wells are drilled, the more that they are being overestimated.”

‘Same Dynamic’

Extrapolating from field studies Montgomery and his colleague Francis O’Sullivan conducted in North Dakota’s Bakken shale deposit, the research suggests that total U.S. oil and natural-gas production from new wells could undershoot the EIA estimate by more than 10 percent in 2020. Things would get progressively worse each year after that as wells in various sweet spots are exhausted and technology fails to close the gap. “The same forecasting methods are used in other plays in the U.S., and the same dynamic is likely to be present,” Montgomery added. Margaret Coleman, the EIA’s leader of oil, gas and biofuels exploration and production analysis, said in an email “the study raises valid points” and the administration is looking at ways to give its estimates a tighter focus. She added that many shale fields lack the detailed well data that informed the MIT study, which means EIA forecasters have to use known geologic information and assumptions about prices and technology to come up with estimates.OPEC’s Epic Battle Against Shale -- A QuickTake

There’s little doubt the technologies used to extract oil and natural gas trapped within rock formations thousands of feet below the Earth’s surface -- like drill heads, mapping software, fracking techniques and so on -- have gotten better. And intuitively, it makes a lot of sense that better methods have boosted U.S. shale output and helped lead to new finds. “It’s really hard to bet against the ability of the industry to improve and get more out of the rock,” said Manuj Nikhanj, co-chief executive officer of RS Energy Group.Undisputed Leader?

Just last month, International Energy Agency Executive Director Fatih Birol said shale production will make the U.S. the “undisputed leader of global oil and gas markets for decades to come.” But if the MIT researchers are ultimately right, the implications could be significant. In the past three years, oil prices have been stuck around $50 a barrel on the back of rising shale output in the U.S., while natural gas has been selling for an average of less than $3 per million British thermal units. (As recently as 2014, prices for both were twice as high.) Not only could a slowdown in production mean higher energy prices, but it also might just mark the end of the U.S. shale industry’s role as the one swing producer able to counter OPEC’s might. The shale boom has repeatedly frustrated the Saudi-led cartel’s attempts to control oil prices. As recently as 2015, OPEC tried to pump its U.S. rivals out of business, only to blink after shale drillers adapted by reducing costs. On Thursday, the Organization of Petroleum Exporting Countries and its allies agreed to maintain oil-output cuts through 2018, extending a campaign to wrest back the global market from America’s shale industry.Power Struggle

President Donald Trump himself has talked up “energy dominance” as a key policy, with U.S. oil and gas helping supply the world’s power needs. Of course, the MIT researchers aren’t the first to question the projected growth of U.S. shale. Analysts have long debated varying methods used to predict output. And unsurprisingly, the Saudis have cast doubt on how long the shale boom can last. Even billionaire oilman Harold Hamm recently slammed what he considered EIA’s “exaggerated” forecasts, saying they’re depressing U.S. oil prices. (After all, higher prices are better for the bottom line.) Yet, MIT’s findings stand out by providing some evidence that backs those assertions. The problem with the EIA’s numbers, the researchers say, is that they give drillers too much credit for coming up with ways to improve fracking. While the EIA’s model assumes that technical advances -- such as well length and the amounts of water and sand used in fracking -- increase output at new wells by roughly 10 percent each year, MIT findings from the Bakken region suggest it’s closer to 6.5 percent, according to Montgomery. Increasing productivity of each new well matters because it’s the only way to boost output. Typically, production drops precipitously soon after a well is tapped. The EIA recently estimated about half of U.S. oil output came from wells two or fewer years old.Field of Dreams

So even though output in the Bakken more than tripled from 2012 to mid-2015 on a per-well basis, MIT’s research suggests the main reason is that shale companies abandoned iffier fields to drill in the best acreage following the slump in energy prices. “There certainly could be some validity to getting a rosier forecast because right now, the industry is working sweet spots,” said Dave Yoxtheimer, a hydrogeologist at Penn State University’s Marcellus Center for Outreach and Research. “When that’s all played out, they’re going to have to go to the tier-two acreage, which isn’t going to be as productive.” Indeed, some signs of a slowdown have started to emerge. Gas output in the Marcellus basin has fallen 10 percent on a per-rig basis since reaching a high in September 2016. In the Permian, per-rig oil production has decreased almost 20 percent over a similar span. Richard Bereschik knows firsthand that shale isn’t a sure thing. The bearded, burly superintendent of schools in Wellsville, Ohio -- a small, Rust Belt community located along the western bank of the Ohio River -- recalls the rush he and other townsfolk experienced when Chesapeake Energy Corp. came through some six years ago, leasing out huge tracts of property for development. Wellsville sits atop the Marcellus and Utica shale formations and is only 20 miles from a concentration of sweet spots, but Bereschik says Chesapeake stopped renewing leases after the bottom fell out in prices. “Everyone thought we’d found a goose that laid the golden egg,” Bereschik said. But ultimately, “it’s not the boom we all expected.” Joseph Barone President Shale Directories, LLC www.shaledirectories.com jbarone@shaledirectories.comThursday, November 30, 2017

Unit Corp. Appoints Les Austin As CFO, SVP

Unit Corp. (NYSE: UNT) said Nov. 27 it had named Les Austin as senior vice president and CFO of the Tulsa, Okla.-based company effective immediately.

Austin, age 51, has more than 23 years of energy finance and leadership experience, according to the company release. He replaces David T. Merrill, who held the position of CFO at Unit until he was promoted to COO in August.

Through its subsidiaries, Unit is focused on oil and natural gas exploration, production, contract drilling and natural gas gathering and processing.

Source: Daily Dose of ShaleDirectories.com News

Source: Daily Dose of ShaleDirectories.com News

https://www.shaledirectories.com/blog/unit-corp-appoints-les-austin-as-cfo-svp/

Monday, November 27, 2017

Keystone To Resume Crude Oil Deliveries

TransCanada Corp. (NYSE: TRP) said Nov. 27 that its Keystone Pipeline repair and restart plans have been reviewed by the Pipeline and Hazardous Materials Safety Administration (PHMSA) with no objections, permitting a safe and controlled return to service of the Keystone system.

Source: Daily Dose of ShaleDirectories.com News

Source: Daily Dose of ShaleDirectories.com News

https://www.shaledirectories.com/blog/keystone-to-resume-crude-oil-deliveries/

Sunday, November 26, 2017

OPEC Played Cutbacks Well, Now What?

The Nov. 30 meeting of OPEC could have a dramatic impact on already volatile crude oil prices. How things play out for crude in 2018 remain to be seen.

Jeff Quigley, director of energy markets for Stratas Advisors, will attend that meeting in Vienna and outlined key drivers that must be considered as the cartel’s members mull its efforts to rein in supply in a Nov. 16 presentation at Hart Energy’s DUG Eagle Ford conference.

“The market shifts have been incredible,” Quigley noted, and that could make the meeting contentious. “Markets now have a very bullish mindset, OPEC could not have written the script any better. But mindsets turn on a dime” while the actual market can’t move that quickly.

Source: Daily Dose of ShaleDirectories.com News

Source: Daily Dose of ShaleDirectories.com News

https://www.shaledirectories.com/blog/opec-played-cutbacks-well-now-what/

Friday, November 24, 2017

Icahn takes big stake in SandRidge Energy

Independent oil and gas producer in 2016 survived a Chapter 11 bankruptcy filing, and came out on the other side strong enough to last week announce a $746 million acquisition of a fellow producer.

Source: Daily Dose of ShaleDirectories.com News

https://www.shaledirectories.com/blog/icahn-takes-big-stake-in-sandridge-energy/

Thursday, November 23, 2017

8 major producers commit to reduce methane emissions

BP, Eni, ExxonMobil, Repsol, Shell, Statoil, Total and Wintershall this week committed to further reduce methane emissions from natural gas assets they operate around the world, Kallanish Energy reports.

Source: Daily Dose of ShaleDirectories.com News

https://www.shaledirectories.com/blog/8-major-producers-commit-to-reduce-methane-emissions/

Wednesday, November 22, 2017

USGC Petrochemical Supply Chain Industry Set to Meet in Houston Dec 12-13

The 3rd annual Petrochemical Supply Chain and Logistics Conference is being held this year at the Royal Sonesta Hotel, December 12 – 13, 2017. The theme this year is ‘Delivering Supply Chain Excellence Amid Petrochemical Growth’, and with over 700 attendees expected over two days, this ever-growing event will unite the entire gulf coast petrochemical supply chain community for two days of networking and knowledge sharing.

With senior Supply Chain Directors from the likes of BASF, Formosa Plastics and Hunstman Corporation confirmed to speak, the agenda will focus on optimizing the domestic supply chain, understanding how the digital supply chain affects the petrochemical industry, assessing the impact of hurricane Harvey on supply chain logistics, and more.

Key Themes at Petrochemical Supply Chain and Logistics 2017:

- Assessing Harvey’s True Impact

- Understanding the Real Implications of New Volumes & Anticipate Producer Supply Chain Needs

- Generating Capacity to Keep Up with Export Demand

- Optimizing the Domestic Supply Chain: Capitalize on Distribution at Home

- The Future Is Digital: What Does a Digital Supply Chain Mean for Petrochemicals?

Subscribe to:

Posts (Atom)